An Endowment is not a "rainy-day" fund

Correcting a common and very annoying (at least to me) misconception of about endowments

I recently listened to Sam Harris’s interview with Greg Luckianoff. It was a good interview, but one thing really annoyed me! Near the end of the conversation, Greg, speaking about his nephew who will be starting college soon, (not unreasonably) complains about how absurdly high headline tuition rates have gotten and suggests that colleges need to cut down on administrative bloat. I agree! But then he adds, presumably referring to the endowment fund of whatever prestigious college his nephew is planning to attend, “especially given that he’s looking at a school that has, you know, $60 billion in its rainy-day fund”. But, and this is very important, an endowment is absolutely nothing like a “rainy-day fund”!

This isn’t the first time Sam has demonstrated his total misunderstanding of what an endowment is. Back in 2020, shortly after the onset of covid lockdowns, Sam complained about Harvard’s decision to lay off some of its non-academic staff in response to lockdowns during an interview with Caitlin Flanagan (I referenced this podcast in the first ever video of my short Youtube career). As a result of campus shutdowns, Harvard had chosen to lay off some of their janitorial, food service and other staff whose jobs had been made temporarily irrelevant. Sam, shocked by what he saw as Harvard’s disregard for the concerns of their most vulnerable staff members, hysterically referred to this as a “reputation canceling event”, with his sense of outrage closely tied to their massive endowment size.

What is an endowment?

But it would have been irresponsible, and one could even argue technically imprudent, for Harvard to have used their endowment to fund the incomes of these temporarily unneeded staff, especially given the state of their endowment assets and expected revenues at the time. To understand why, and more generally why colleges don’t use their endowment funds in the exact way outside commenters assume they should, you have to actually know what an endowment is! So, very simply, an endowment fund is a specially regulated pool of capital which exists to support an institution in serving its mission in perpetuity. (Sometimes endowments have a finite duration, but in the case of colleges and universities they are generally intended to be permanent pools of capital.) In most states endowment funds are subject to the Uniform Prudential Management of Institutional Funds Act (UPMIFA) which provides “uniform and fundamental rules for the investment of funds held by charitable institutions and the expenditure of funds donated as endowments to those institutions”.

An endowment is not a rainy-day fund that sits there waiting to be dipped into whenever the university has cash flow problems (although it can occasionally serve that purpose, within limits). Instead, the endowment is a pool of money from which an annual spend is taken to support general operating expenses, or in some cases specific incentives (some donors give “restricted” gifts to the endowment). The endowment assets are invested with the goal of making large enough returns over time to keep up with both annual spending and inflation. The intention is to maintain “intergenerational equity”, in other words to keep the endowment, in real terms, at least as large as it is now in perpetuity without accounting for any future donations. At schools with very large endowments the annual spend is able to cover a significant portion of operating costs – for example: in fiscal year 2021, 39% of Harvard’s operating revenue came from endowment income vs. only 17% from student income.

Endowment Management

The original endowment capital comes mainly from wealthy donors, often alumni who want to give back to and/or raise the prestige of their alma mater. For instance, Michael Bloomberg, has given at least 3.5 billion to Johns Hopkins University, which massively increased their endowment size and has enabled additional research, particularly in the area of Public Health. This capital is then managed by asset management professionals either internally, as is the case for those, such as Harvard or Yale, which have very large endowments, or externally for most others – either by asset management teams within banks, through consultants, or via specialized asset managers.

Such specialized asset managers provide services specifically for endowments and foundations, serving university endowments which are not large enough to maintain an asset management staff, and whose AUM is too small to enable them to write large enough checks (on their own) to get access to the most sought-after private equity and hedge funds. These asset managers work with their clients to determine asset allocation targets in line with their risk and return goals, allocate their capital to various fund products and pool it with the funds of other endowments so that they could access much more diverse and higher-quality fund managers than they could have on their own.

As I mentioned above, the main goal of endowment asset management is to achieve “intergenerational equity”, which means that after the annual spend and inflation are considered, the endowment assets grow at a fast enough average pace such that their real value is not degraded over time. You also want to invest in a diversified portfolio so that the growth is relatively consistent over time, since most schools rely on their annual endowment spend and taking a large spend when assets are in drawdown makes recovering very difficult, as will be discussed later. Typically, annual spending is approximately 5% of the endowment assets, so this goal is often referred to as “CPI+5” for short. CPI+5 refers to an annual total return target of inflation (as measured by the consumer price index) plus 5%.

Endowment Spending

The roughly 5% spending target is generally considered to be reasonable, since CPI+5 is seen as an achievable long-term return target that doesn’t require excessive risk taking, but the institution can spend more or less than that so long as they can defend its “prudence”. In some states, such as California, spending above 7% of the endowment value is “presumptively imprudent”. The annual endowment spend must also be used to support the purpose of the institution rather than to fund any random initiative as it must be aligned with donor intent and organizational mission.

When Sam called Harvard’s choice to lay off lower income staff members a “reputation cancelling event” his frustration was driven by what he interpreted as their hypocrisy given that he and Caitlin viewed Harvard as an “explicitly far-left organization” which therefore should be more concerned about the incomes of their low-skilled employees than they are their bottom line. I can somewhat understand where this feeling came from, but he was still wrong to be so confident when claiming Harvard’s large endowment should have been spent for this purpose.

Something to keep in mind is that at the time of this decision, the markets had not yet recovered from the covid crash, so endowment assets were significantly down. In addition, Harvard may have been facing higher than normal uncertainty about expected revenues, and so it would be sensible for them to try to reduce expenses where they could in anticipation of that. Sure, they could make the case that they needed to draw a larger than standard percentage of the endowment for current spending to make up for lost revenues, but it’s not obvious they should, particularly when you consider the impact on ability to recover from the drawdown which favors spending less (if you can) when assets are down.

To see why consider the following example:

Annual spend is generally calculated using some variation of a moving average of total assets over the past 3-5 years. Say Harvard used a 3-year moving average and a 5% spend target. Assume that as of April 2020 total assets were down 25% from end of 2019, and that the assets at end of 2019 been exactly flat vs. year end 2018. Then if Harvard chose to spend 7.5% of the moving average of their assets this year, to make up for hardships etc., rather than 5%, they’d end the year, they’d finish the year with 68.1% of the assets they’d had in 2019 rather than 70.4%. And in order to get back to the nominal asset value they had as of end of 2019 they’d have to make a total return of 46.8% rather than 42.0%, making recovering from this large drawdown, a necessity if they’re to achieve the goal of maintaining intergenerational equity, even more difficult.

But more fundamentally, to draw a larger than normal spend the case would have to be made that this was a prudent choice in light of the ability of Harvard to fulfill their mission in the long-term. As I mentioned, endowment funds must be spent in service of the mission of the organization and in line with donor intent. Since Harvard’s mission is “to advance new ideas and promote enduring knowledge”, it's far from clear that paying to keep unneeded staff would’ve been in service of that.

What are students actually paying?

On that note, I thought I’d also briefly respond to Greg’s complaint about tuition fees. First, I agree that tuition fees are crazy high, that they’ve increased far faster than inflation over the past several decades, and that reducing administrative costs which have ballooned over the same period would be a good thing. But when people quote the sticker price of tuition at elite universities it’s important to know that very few students actually pay that amount. Data from the National Center for Education Statistics shows that 81% of full-time, full-year undergraduates received financial aid for the 2020-2021 school year with the average amount being $22,000.

College tuition is sensitive to income and ability – rich students pay more all else equal, but schools also want to attract the best students and will offer discounts on that basis. The process of determining who gets in is much more complicated than you might think. Before I worked in this industry, I naively assumed that colleges more or less looked at all the applications they got, determined which ones were the best and how many spots they had available, and then sent offers to those students, and offered discounts to some on the basis of need. I was also aware that students were often offered discounts on the basis of test scores or experience as a way to lure the best students to their school, but I didn’t think about it too much.

In fact, the process is more complex. Many colleges even hire “Financial Aid Optimization Consultants” to determine a mix of offers and tuition reimbursements intended to maximize the overall quality of the students who will accept while meeting a predetermined revenue target. Basically, you need to let in enough kids of mediocre quality who will accept and can pay full price so that they can subsidize the tuition of smart kids who can’t pay or who wouldn’t accept the offer if they did have to pay. For each student, their chance of accepting an offer given varying levels of tuition discounts is taken into account so that the overall expected tuition revenue and student body make up can be estimated for a given set of offer letters.

If a school wanted to maximize the quality of the students they admitted and didn’t require tuition revenue, they would offer full tuition reimbursement for all students and send offers to only the best students that applied. This would maximize their chance of getting each of these students to accept and reduce the degree to which they had to send offers to students further down in the pile. Of course, they don’t do this because, especially smaller schools, rely on that tuition revenue for operations. The main point is that expected revenues are a part of the admission process, and for good reason, but to read more about this check out this NY Times interview with Angel Perez of Trinity College.

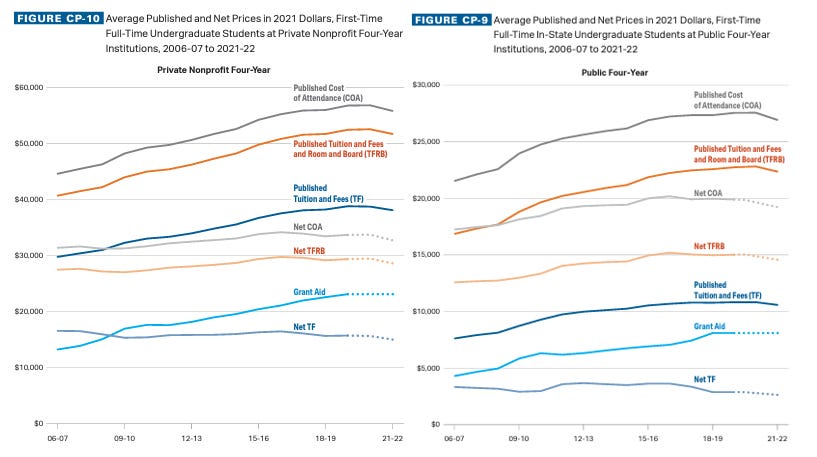

Between the 2006-2007 and 2020-2021 school years, according to data from the College Board, the published cost of attendance at both private and public colleges increased significantly on an inflation-adjusted basis but the net cost of attendance, which accounts for grant-aid has been roughly flat. What we’ve seen then, is a greater variation in tuition paid by different students at the same school as grants have increased in tandem with sticker tuition prices. What this means is that we likely have a more progressive system of tuition costs, with the wealthier students more fully subsidizing the less wealthy students, or the particularly high-quality students.

Again, this isn’t to say that college attendance costs are “reasonable” or that they haven’t risen over a longer period of time, but that the published cost of attendance overstates the actual cost, and hides the degree to which wealthy kids fund the education of poorer kids. Perhaps if people could internalize that this is how it works – smarter poorer kids maintain the reputation of the school while reasonably but not as smart wealthy kids fund everyone’s education – they would be less outraged about things like legacy admissions.

So, to conclude, yes, schools have large endowments, so large in some cases such that they need to hire entire offices of internal asset management professionals to manage them. But, the endowment growing over time is not a sign of a schools greed but is exactly how an endowment is supposed to work, maintaining itself over time after a small spend is taken each year such that it can continue to provide the same level of support (adjusted for inflation) in perpetuity. The endowment spend is used to fund things that serve the mission of the college, including tuition reimbursements and general operating expenses, but cannot be used to fund general charitable causes, nor can it be spent at an imprudent pace.

Wow, I never suspected that there would be so much to know about endowments. I thought being envious and resentful would suffice. Thank you.

If people knew enough about personal finance to be familiar with the 4% rule, the endowments would be much more widely understood. It’s the same damn thing.